Tuesday, 21 July, 2026

Bhutan has maintained a strong economic growth trajectory over recent decades, averaging 7.5% annually since the 1980s, underpinned by public sector investment in hydropower and robust performance in the service industry, particularly tourism.[1]

According to the World Bank's May 2025 Bhutan Development Update, Bhutan's real GDP grew by 4.9 per cent in FY2023/24, driven by the service sector—particularly tourism, financing, insurance, and real estate—alongside growth in mining and quarrying. The economy is projected to accelerate to 7.0 per cent in FY2024/25,recording the highest growth rate in South Asia, supported by the commissioning of new hydropower plants and expansion of non-hydropower exports.[1]

Bhutan's nominal GDP stood at approximately USD 3.41 billion in 2025, according to Worldometer estimates, with per capita GDP rising to USD 4,245 in 2024 as reported by Bhutan's National Statistics Bureau—a marked increase from USD 3,491 recorded in 2022—placing Bhutan among the higher per capita income economies in South Asia.[2],[3]

Growth has also translated into meaningful poverty reduction. Extreme poverty based on the USD 2.15/day benchmark has been eliminated as of 2022, and the share of the population living below the USD 6.85/day poverty line declined sharply from 39.5 per cent to 8.5 per cent between 2017 and 2022.[4]

A landmark development in December 2023 was Bhutan's graduation from the United Nations' list of Least Developed Countries (LDCs), making it only the seventh country to achieve this milestone. Bhutan's 13th Five-Year Plan (2024–2029) focuses on attracting foreign direct investment, expanding the private sector, and establishing the Gelephu Mindfulness City—an ambitious special administrative region intended to diversify the economy beyond hydropower.[5]

Inflation has been brought under control, declining from 7.4 per cent in 2021 to 2.8 per cent in 2024, though food price pressures remain due to Bhutan's close economic linkage with India through the pegged Ngultrum. Youth unemployment stood at a concerning 19 per cent in 2024, with ongoing emigration of skilled workers posing medium-term risks.[1]

Bhutan stands out as a global leader in harnessing renewable energy. Its primary source of energy is hydropower, accounting for nearly 100% of its electricity generation4w3uyf. This reliance on hydropower contributes significantly to Bhutan's economic development, environmental sustainability, and commitment to renewable energy

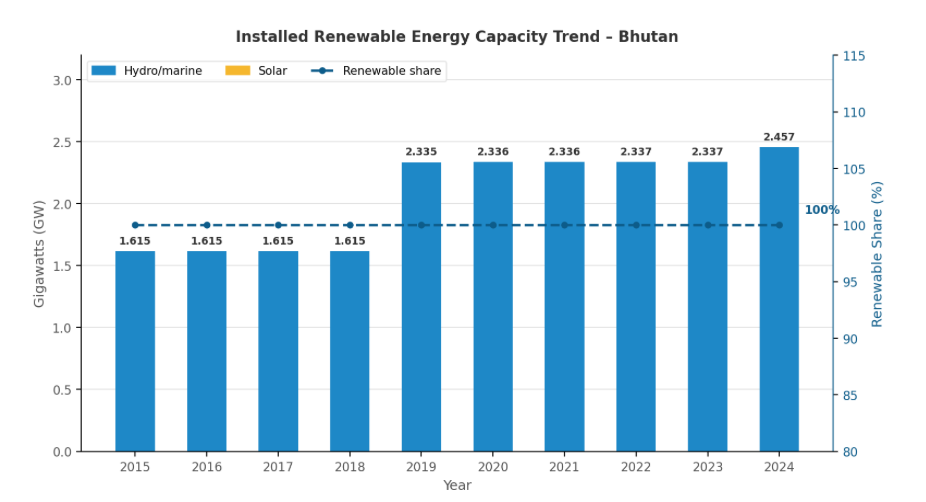

Fig. 1: Installed Renewable Energy Capacity Trend – Bhutan, 2015–2024 (GW). Data source: IRENA Renewable Capacity Statistics 2025 [11]; MoENR Bhutan [12]. Renewable share maintained at 100% throughout.

Bhutan's hydrogen trade profile, whilst still modest in scale, reflects the country's nascent engagement with hydrogen as a commodity. According to the Observatory of Economic Complexity, [6] Bhutan exported USD 35.2k in hydrogen in 2021, primarily to India, ranking it as the 121st largest hydrogen exporter globally. In the same year, Bhutan imported USD 66.3k in hydrogen from India. These figures represent conventional hydrogen trade and predate the country's formal strategic pivot towards green hydrogen.

The broader aspiration lies in Bhutan's National Hydrogen Roadmap (2024), which envisages transforming the country from a minor hydrogen trader into a regional green hydrogen producer and exporter. By 2030, annual green hydrogen production is targeted at 53,418 tonnes, scaling to an ambitious 428,207 tonnes per year by 2050. The roadmap was formally launched on 24 July 2024 in Thimphu, following its introduction at the COP28 climate summit in Dubai in December 2023.

Bhutan, a nation synonymous with sustainability and Gross National Happiness (GNH), has made substantial strides in formalising its hydrogen policy since the earlier 2023 roadmap concept. The National Hydrogen Roadmap (2024), published by the Ministry of Energy and Natural Resources (MoENR), [9] provides a comprehensive strategic framework for developing a green hydrogen economy powered by the country's abundant hydropower resources.

The roadmap is structured around three strategic phases:

Key quantified targets embedded in the policy include:

Bhutan's National Energy Policy 2025 (NEP 2025), approved by Cabinet on 5 June 2025 and published by MoENR, [10] formally integrates green hydrogen into national energy planning. The policy sets a green hydrogen production target of 70,000 tonnes by 2050 and references the Hydrogen Roadmap 2024 as its guiding instrument. NEP 2025 supersedes several earlier frameworks, including the Sustainable Hydropower Development Policy (2021) and the Alternative Renewable Energy Policy (2013), consolidating Bhutan's energy strategy under a single, forward-looking document.

To attract investment and de-risk the sector, Bhutan is building an investment-friendly regulatory and fiscal framework that includes tax incentives, import duty waivers, subsidies, and pathways for joint ventures with international technology partners. The United Nations Development Programme (UNDP) is an active collaborating partner, having co-organised a 2024 stakeholder consultation on green hydrogen potential alongside MoENR. [8]

Bhutan's hydrogen regulatory environment is progressing from the nascent stage it occupied in early 2024 towards a more structured framework, shaped largely by the policy actions taken since the National Hydrogen Roadmap's formal launch.

Current Landscape

Expected Outcomes

The combined force of NEP 2025 and the Hydrogen Roadmap is expected to culminate in a comprehensive hydrogen regulatory framework encompassing:

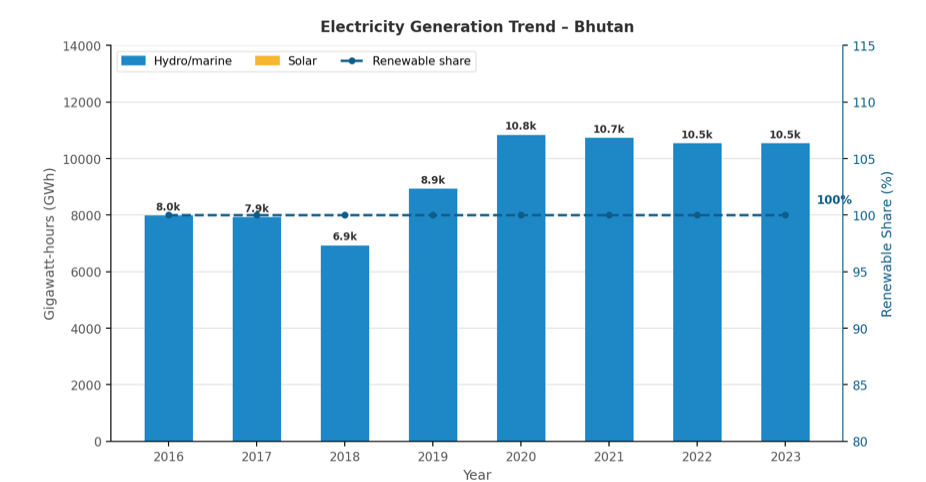

Bhutan's renewable energy endowment is substantial, though the full potential remains largely untapped. According to the IRENA Renewable Capacity Statistics 2025, [11] Bhutan's total installed renewable capacity reached 2,456 MW by end of 2024, up from 2,336 MW in 2023, with almost the entirety being hydropower. IRENA's Bhutan country profile records total electricity generation of 10,536 GWh in 2023, of which 100 per cent was renewable—10,535 GWh from hydro and marine sources and 1 GWh from solar. [12]

Hydropower

Hydropower is the cornerstone of Bhutan's energy system. The country possesses a theoretical hydropower potential of 32,600 MW, of which approximately 30,000 MW is techno-economically viable. [13] Currently, installed hydropower capacity stands at 2,336 MW, meaning only a fraction of the total potential has been harnessed. The generation profile has grown substantially since 2019, when the commissioning of the 720 MW Mangdechhu project raised total capacity by approximately 45 per cent in a single step. [14]

In a landmark development, Adani Power and Druk Green Power Corporation (DGPC) signed a Shareholders' Agreement and Concession Agreement on 6 September 2025 for the 570 MW Wangchhu Hydropower Project. [15] This is the first major project under a broader 5,000 MW partnership between Adani Group and DGPC formalised in May 2025, with construction expected to commence in 2026 and a five-year development timeline.

Additionally, in November 2025, Prime Minister Tobgay attended the signing of Commercial Agreements between DGPC and Tata Power for the 1,125 MW DorjilungHydroelectric Power Project, with the World Bank Group as lead financier. Tata Power had earlier acquired a 40 per cent stake in the 600 MW KholongchhuHydropower Project in July 2025, with financing of approximately USD 580 million secured from India's Power Finance Corporation. [16]

Bhutan's overall generation capacity target is 25,000 MW by 2040, comprising 15,000 MW from hydropower and 5,000–6,000 MW from solar energy, as established under NEP 2025. [10]

Fig. 2: Electricity Generation Trend – Bhutan, 2016–2023 (GWh). Data source: IRENA Bhutan Asia Renewable Energy Statistical Profile 2024 [12]. Renewable share maintained at 100% throughout.

There is currently no large-scale domestic manufacturing capacity specific to hydrogen technology in Bhutan. The country's green hydrogen strategy is built primarily around utilising surplus hydroelectric power for electrolysis, leveraging imported electrolysertechnology initially. The National Hydrogen Roadmap envisages partnership with international engineering firms and global technology providers to bring expertise and equipment to Bhutan.[9] An early-stage pilot, co-developed with UNDP support, is expected to begin with a 1 MW electrolyser facility, scaling to 5 MW with on-site hydrogen refuelling infrastructure.[8]

In the broader energy technology space, NEP 2025 promotes the adoption of AI-based grid management, smart meters, digital twin systems, and Distributed Energy Resource Systems (DERS) to modernise the grid in parallel with generation capacity expansion.[10]

Bhutan's project pipeline has transformed considerably since early 2024, transitioning from a landscape of stated intentions to one with concrete agreements and active development timelines. The combination of the National Hydrogen Roadmap (2024), NEP 2025, and major investment partnerships positions Bhutan as an increasingly credible actor in regional clean energy.

Active and Forthcoming Projects

Investment Outlook

The green hydrogen sector will require cumulative investment of USD 8 million by 2030, USD 145 million by 2040, and USD 395 million by 2050.[7] The Royal Government of Bhutan is actively pursuing international development bank financing, bilateral grants, and private sector participation through joint ventures. Fiscal provisions embedded in NEP 2025 and the Hydrogen Roadmap—including import duty waivers, subsidies, and concessional financing—are designed to lower barriers for investors and ensure commercially viable project structures.[7],[10]

Bhutan's combination of constitutional carbon neutrality commitments, proven hydropower expertise, an ambitious and funded regulatory framework, and high-profile industrial partnerships with Adani, Tata, and Reliance make it a distinctly competitive and credible destination for green hydrogen investment in the South Asian region.