Thursday, 30 July, 2026

Renewable energy potential in Indonesia reaches 3,686 GW according to official estimates by the Ministry of Energy and Mineral Resources (MEMR). The highest potential comes from solar energy (3,295 GW), followed by wind (155 GW), hydro (95 GW), tidal (60 GW), bioenergy (57 GW), and geothermal (24 GW) (BPSDM ESDM, 2022).

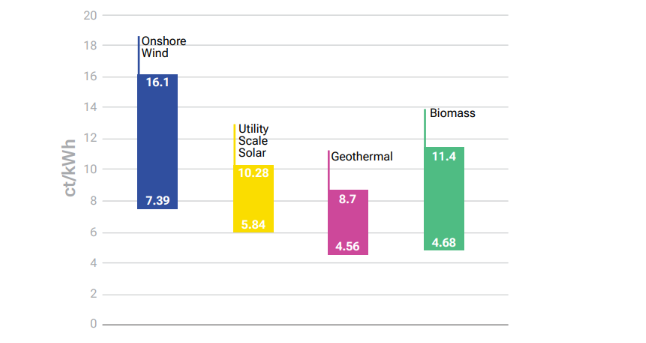

While the solar and wind energy potential are abundant, resources are rather average compared to other countries. For wind energy, the mean power density for the top 2 Percent windiest area in South Sulawesi and East Nusa Tenggara -the best locations in Indonesia- is about 400 W/m2, while in New Zealand, for example, the mean power density for the top 2 Percent area is 3,600 W/m2. For solar energy, the capacity factor ranges from 12 Percent to 18 Percent , while it could reach 25 Percent in the Chilean desert or 23 Percent in the Middle East. The average resources result in relatively high cost of renewable energy.

[1] Hydrogen in Indonesia | Business Indonesia (business-indonesia.org)

An analysis estimated that Indonesia requires blue and green hydrogen of about 4 million tonnes per year in 2025; this number is projected to be more than doubled in 2030 and more than quadrupled in 2040 to 17 million tonnes [1]. Drivers behind the increase are the transportation sector, followed by power generation, ammonia, steel, methanol, refinery, and cement industry.

Green hydrogen development in the Indonesian energy sector will start gradually in 2031 and increase rapidly beyond 2050. Its hydrogen generation capacity will significantly increase by 328 MW from 2031 to 2035, 332 MW from 2036 to 2040, 9 GW from 2041 to 2050, and 52 GW from 2051 to 2060. Such tremendous growth can only be satisfied with huge amounts of investment, which are projected to range from USD 0.8 billion in 2031 to USD 25.2 billion by 2060 cumulatively.

Indonesia has yet to set up necessary policies and regulations to develop its green hydrogen industry. Green hydrogen utilization has only been discussed in the net-zero roadmap set up by the Ministry of Energy and Mineral Resources (MEMR). Nevertheless, there are no official key policy documents on hydrogen development except for a few mentions in the general national energy plan (RUEN). Since green hydrogen production requires renewable electricity, regulations on the electricity sector will also apply to green hydrogen production.

Summary of relevant policy and regulatory framework of green hydrogen development in Indonesia

| Regulation | Title | Description |

|---|---|---|

| Law 30/2007 | Energy Law | Puts the emphasis on energy security, sustainable development, energy resilience, and environmental preservation. |

| Government Regulation No.79/2014 | National Energy Policy (KEN) | Targets an increase of NRE share in primary energy mix to 23% in 2025 and 31% in 2050 |

| Presidential Regulation No.22/2017 | National Energy Plan (RUEN) | Sets up a NRE development plan until 2050, including a general action plan for hydrogen development, such as preparation of regulatory frameworks, technological and manufacturing capacity development, and incentives provision |

| Law No. 30/2009 | Electricity Law | Regulates the electricity sector planning and governance. It also stipulates the prioritization of new and renewable energy. |

| New and renewable energy bill | New and renewable energy bill | Regulates NRE development, including pricing, incentives, etc. In the latest draft, hydrogen is mentioned as a new energy. |

Supporting policies and regulations in different sectors Investment and fiscal policies Carbon pricing and taxation: In 2021, Indonesia stipulated a regulation on Carbon Economic Value (CEV) and incorporated carbon tax into the taxation law. CEV could be implemented in the form of carbon trading, result-based payment, and carbon levy/tax. The carbon tax will be set by the Ministry of Finance at a minimum of USD 2 per kgCO2e. The implementation of carbon tax is currently limited to coal-fired power plants, but is expected to expand to other sectors (i.e. transportation and industry). The timeline for implementation in each sector is developed by the respective ministries. Fiscal incentives for green hydrogen projectsAccording to Indonesia Investment Guidebook, there are several fiscal incentives that green hydrogen projects could potentially benefit from:

Transportation sector policies - Automotive industry roadmap by Ministry of IndustryThe roadmap for the automotive industry by the Ministry of Industry plans for fuel-cell electric vehicles (FCEV) development to take place beyond 2030, after the development of BEV. Luxury tax exemption for fuel-cell vehicles: According to PMK 141/2021, luxury tax is exempted for BEV and FCEV, aimed to foster demand for them. The normal luxury tax rate is 10%-30% of the vehicle initialprice, depending on the CO2 emissions and engine displacement.

Indonesia is an archipelagic country, with different levels of economic development in each island. Currently, most industrial activities, hence energy demand, are located on Java island. For example, Java island currently contributes to 60% of the national GDP and 80% of the national energy demand. Therefore, it is expected that future demand for green hydrogen will mainly come from Java. However, the best locations for renewable energy generation are not always in Java. For example, the area with highest solar power potential is in East Nusa Tenggara, where the year average capacity factor could reach 18%. Meanwhile in Java, the capacity factor in most areas is closer to 15-16%. Similarly, for onshore wind, best potentials are located in South Sulawesi and East Nusa Tenggara. Therefore, inter-island transportation might be needed to transport hydrogen from production sites to demand centers.

With the geographical condition of Indonesia, pipelines could be the cheapest method for most inter-island hydrogen transportations. The distances from Java island as demand center to renewable hotspots such as East Nusa Tenggara and South Sulawesi are less than 1,000 km. Meanwhile, transporting hydrogen from the eastern region such as Maluku and Papua by shipping might be more suitable as they are located relatively further and the seas are deeper. However, reflecting on the existing natural gas transportation that is mostly by shipping, it could also be the case for hydrogen. A deeper research should be conducted to understand the cheapest way to transport hydrogen in Indonesia. Nevertheless, in the short term, shipping for transmission and trucking for local distribution will be the option to go since there is no pipeline infrastructure available or even planned yet. Blending into natural gas infrastructure could be an option for inner island transportation in Sumatra and Java where the infrastructure is more established.

Not Available (NA)

There are a few notable ongoing green hydrogen projects, mostly still in the preliminary phase: